eBay Just Told GameStop to Get Lost. Here's Why This Story Is More Interesting Than It Looks.

A $12 Billion Company Tried to Buy a $48 Billion Company. The Target Said No. The Acquirer Says It's Not Done. eBay's board rejected GameStop's $56 billion takeover proposal this morning in a letter that used the phrase "neither credible nor attractive" — two words that,…

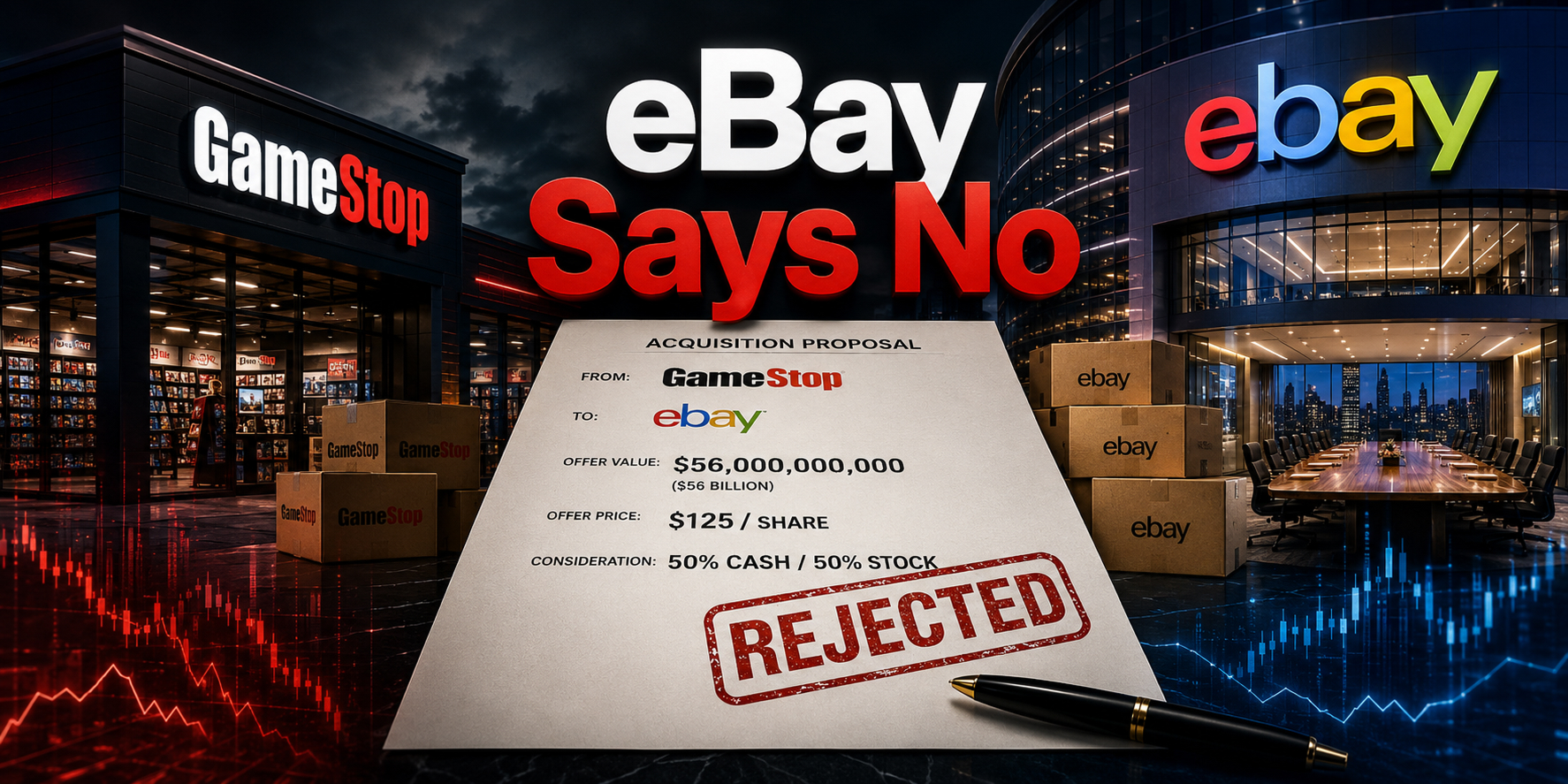

A $12 Billion Company Tried to Buy a $48 Billion Company. The Target Said No. The Acquirer Says It's Not Done.

eBay's board rejected GameStop's $56 billion takeover proposal this morning in a letter that used the phrase "neither credible nor attractive" — two words that, combined, constitute one of the more efficient corporate dismissals in recent M&A history.

GameStop CEO Ryan Cohen said he's prepared to take the offer directly to eBay shareholders. eBay's stock fell 1% on the rejection. GameStop fell 4%.

📋 What GameStop Actually Proposed

GameStop announced the unsolicited, non-binding offer on May 4. The key terms:

- Offer price: $125 per share — a 20% premium to eBay's close on the day of announcement, and a 46% premium to eBay's price on February 4, when GameStop began quietly building a stake

- Structure: 50% cash, 50% GameStop common stock, with full shareholder election rights

- Financing: GameStop reported approximately $9.4 billion in cash and liquid investments as of January 31, 2026, plus a "highly confident letter" from TD Securities for up to $20 billion in debt — contingent on the combined company maintaining an investment-grade credit rating

- Cohen's terms: He would serve as CEO of the combined company, taking no salary, no cash bonus, and no golden parachute — compensated solely on stock performance

- The strategic logic: Use GameStop's 1,600 U.S. retail stores as authentication and fulfillment hubs for eBay orders, cut eBay's bloated $2.4 billion annual marketing budget, and build the combined entity into a credible rival to Amazon

🔢 The Financing Problem, Stated Precisely

The proposal isn't obviously unfinanceable. But the structure has conditions that make it hard to defend on paper.

The offer is half cash, half GameStop stock. GameStop's $9.4 billion in cash and liquid investments plus the $20 billion TD letter gets the deal partway there — but the debt piece is contingent on investment-grade status, and Moody's responded to the announcement last week by saying the deal would be credit negative for eBay. That matters more than it sounds. eBay currently carries an investment-grade credit rating. If the deal triggers even a one-notch downgrade to below Baa3 on Moody's scale — the line separating investment grade from speculative grade — the TD Securities commitment either dissolves or becomes prohibitively expensive to execute. Moody's flagging the deal as credit negative is essentially a pre-emptive warning that the contingency the entire financing structure rests on may not survive the transaction itself. The stock portion covers the remainder, but at GameStop's current market cap of $12 billion, issuing enough shares to cover a multi-billion-dollar gap would be significantly dilutive to existing holders.

GameStop's own shareholders have already pushed back. Michael Burry — who made his fortune spotting the 2008 housing bubble — called the deal strategy "pedestrian" and flagged the debt burden and dilution risk.

Cohen appeared on CNBC's "Squawk Box" dressed in a black leather jacket and T-shirt and did not offer much explanation on how GameStop would finance the $56 billion purchase price. When pressed, he said the deal would be paid for with cash and stock. His short answer prompted awkward silences in the interview.

🤔 So Why Did Cohen Do This?

The financing structure has real questions. The strategic rationale is debatable. The board has rejected it in writing. And yet Cohen has said he'll go directly to shareholders. There are three possible explanations, and they are not mutually exclusive.

The genuine strategic bet. Cohen built Chewy from scratch and sold it for $3.35 billion. He turned GameStop from a dying mall retailer into a cash-rich, debt-free entity looking for a purpose. His thesis — that eBay's cost structure is bloated, its marketing ROI is poor, and its physical footprint opportunity is underexploited — is not unreasonable. eBay spent $2.4 billion on sales and marketing in fiscal 2025 and added exactly one million net active buyers. That is $2,400 per new buyer. Cohen is not wrong that there's fat to cut.

The narrative play. GameStop's stock has historically responded to attention and momentum as much as fundamentals. A hostile takeover attempt against one of the most recognizable brands in e-commerce generates significant coverage and reinforces the kind of narrative momentum that has historically mattered for GameStop's valuation. A bid that fails on deal terms but succeeds in keeping the story alive is not automatically a wasted effort.

The activist unlock play. eBay has been trading well below analysts' estimates of intrinsic value for years. If Cohen's bid forces eBay's board to articulate and execute a credible standalone value creation plan — or opens the door to a better-capitalized acquirer — GameStop's stake in eBay stock, accumulated since February 4, becomes considerably more valuable. Activists have used similar "bid to unlock" strategies before.

📍 Where Things Stand

eBay has rejected the bid. Cohen has threatened a hostile approach — taking the offer directly to eBay shareholders, possibly calling a special meeting.

For a hostile bid to succeed without board support, Cohen would need to convince a majority of eBay's shareholders to tender their shares at $125 — a price eBay's stock is currently approximately 17% below. He would need to demonstrate financing that addresses the contingencies the TD letter does not resolve. And he would need to do it against structural defenses that make hostile takeovers considerably harder than simply winning a shareholder vote.

eBay operates with a classified board structure — meaning board members serve staggered multi-year terms, with only a portion up for election in any given year. That means even if Cohen called a special meeting and won a shareholder vote to replace board members, he could not replace the entire board at once. Taking control of eBay through a proxy fight is a multi-year process, not a single vote. eBay also retains the right to adopt a shareholder rights plan — commonly known as a poison pill — if the board determines it is necessary to protect shareholders from a coercive or inadequate offer. The board has not adopted one yet, but the threat of doing so is itself a deterrent to a hostile approach.

The board rejection and Cohen's vague CNBC answers make the bid harder for even enthusiastic shareholders to defend on financial grounds. The more likely outcome is that the bid either dies here or becomes a pressure campaign rather than a completed takeover — with the real value accruing to GameStop's eBay stake if the pressure forces strategic action at eBay rather than a deal close.

💼 What This Means for Investors

eBay (EBAY): Trading around $107 — approximately 17% below the $125 offer price. The discount reflects the market's skepticism that the deal closes. If it definitively does not, eBay returns to trading on its own fundamentals, which its turnaround narrative has been building a case for. The bid did eBay one accidental favor: it forced the company to publicly defend its standalone value creation plan, which is exactly the kind of pressure that can accelerate execution.

GameStop (GME): Down 4% this morning. The more important investor question is not simply what Cohen does next — it is what this bid reveals about his strategic intentions. Is this discipline, showing that he'll swing at big targets when he sees mispriced assets? Desperation, showing that a cash-rich company with no obvious business plan reaches for something it cannot credibly finance? Or a deliberate use of GameStop's meme-stock equity as acquisition currency — a playbook that has no established precedent in corporate history but is not obviously irrational given GameStop's unusual shareholder base?

The broader M&A market: A $12 billion company attempting a hostile takeover of a $48 billion target using meme-stock equity as partial currency is either a creative financing innovation or a sign that the meme era never really ended — it just went quiet for a while. Either way, the outcome will establish precedent for whether retail-driven equity can function as credible M&A consideration.

Sources

- CNBC — "eBay rejects GameStop's $56 billion takeover bid, calling it 'neither credible nor attractive'": https://www.cnbc.com/2026/05/12/ebay-rejects-gamestops-takeover-ryan-cohen.html

- Reuters / Yahoo Finance — "eBay rejects GameStop's $56 billion bid as 'neither credible nor attractive'": https://finance.yahoo.com/markets/stocks/articles/ebay-rejects-gamestop39s-56-billion-bid-as-39neither-credible-nor-attractive39-100427961.html

- Bloomberg — "eBay Rejects GameStop's $56 Billion Takeover as Not Credible": https://www.bloomberg.com/news/articles/2026-05-12/ebay-rejects-gamestop-s-56-billion-takeover-as-not-credible

- Investing.com — "eBay rejects GameStop's controversial $56bn takeover bid": https://www.investing.com/news/stock-market-news/ebay-rejects-gamestops-controversial-56bn-takeover-bid-shares-fall-4679633

- BNN Bloomberg — "eBay rejects GameStop's audacious US$56 billion takeover bid": https://www.bnnbloomberg.ca/business/2026/05/12/ebay-rejects-gamestops-audacious-us56-billion-takeover-bid/

- CNBC — "GameStop stock sinks after surprise eBay takeover bid, Cohen's combative CNBC interview": https://www.cnbc.com/2026/05/04/gamestop-ebay-takeover-bid-ryan-cohen-gaming-retail-ecommerce.html

- SEC EDGAR — GameStop Corp. Form 8-K, Exhibit 99.1 (eBay Proposal Letter): https://www.sec.gov/Archives/edgar/data/0001326380/000119312526202468/d138475dex991.htm

Market Munchies and Mode Mobile communications are for informational purposes only, and are not a recommendation, solicitation, or research report relating to any investment strategy, security, or digital asset. All investments involve risk including the loss of principal and past performance does not guarantee future results.

Any information contained in this commentary does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no guarantee that any statements or opinions provided herein will prove to be correct.