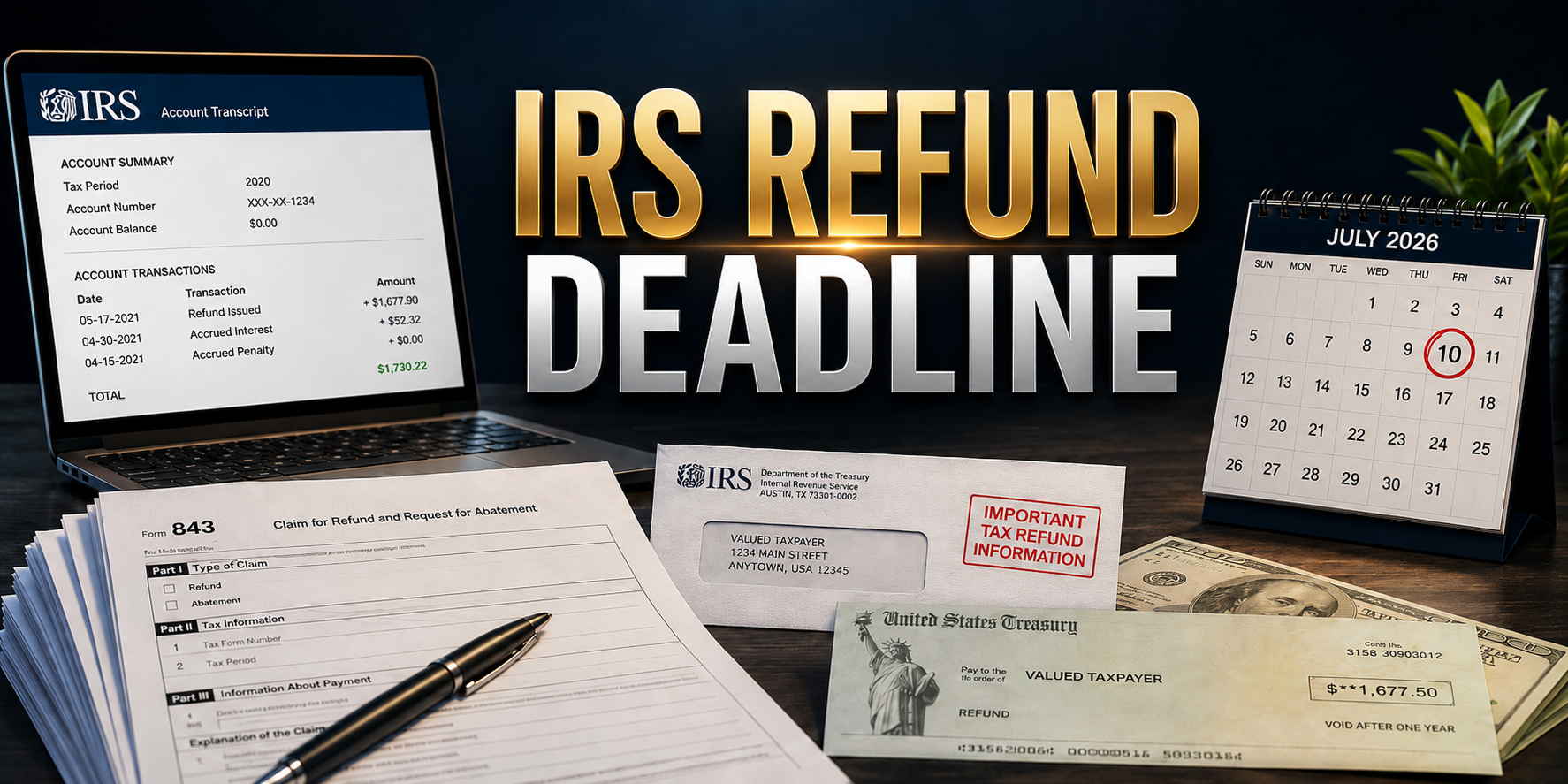

The IRS May Owe You Money From the Pandemic. Here's How to Find Out — and How to Claim It Before July 10.

A Court Ruling Could Open the Door to COVID-Era IRS Penalty Refunds. The Money Won't Come Automatically — and Most Taxpayers Have Until July 10 to Protect Their Claim. A federal court recently ruled in a way that could mean the IRS was not entitled to charge late filing and…

A Court Ruling Could Open the Door to COVID-Era IRS Penalty Refunds. The Money Won't Come Automatically — and Most Taxpayers Have Until July 10 to Protect Their Claim.

A federal court recently ruled in a way that could mean the IRS was not entitled to charge late filing and payment penalties for much of the pandemic period — and if you paid those penalties, a court ruling may create a refund claim worth pursuing.

The catch? It won't happen automatically. You have to ask. And most people have until July 10, 2026 to do it. The ruling is also still being litigated — the Treasury Department disagrees with it — so nothing is guaranteed yet.

🔍 What Actually Happened

The issue starts with a court case called Kwong v. United States, decided in November 2025 by the U.S. Court of Federal Claims.

The court read the disaster-relief statute to postpone many federal tax filing and payment deadlines during the COVID disaster period, rather than only the deadlines the IRS had formally extended. Under that reading, no tax filing or payment was actually "late" from January 20, 2020, through July 10, 2023 — the full pandemic disaster period plus an extra 60 days.

If that interpretation holds up, then penalties charged for late filing or late payment during that stretch may have been improper. The Treasury Department disagrees with the ruling and the case is still being litigated — so there's no guarantee of a refund. But the deadline to preserve your right to claim one is July 10, 2026, and if you miss it, you may permanently lose the ability to claim a refund even if the ruling eventually holds in taxpayers' favor.

🙋 Do You Qualify?

You might qualify if any of the following happened between January 20, 2020, and July 10, 2023:

- You filed a tax return late and were charged a failure-to-file penalty (typically 5% of your unpaid taxes per month, up to 25%)

- You paid your taxes late and were charged a failure-to-pay penalty (0.5% of your balance per month, up to 25%)

- You were charged interest on a late payment or unpaid balance during that period

- You paid estimated tax penalties — common for self-employed people and small business owners

- You filed a late international information return (these can carry large penalties even when no tax is owed)

This applies to individuals, small businesses, large corporations, estates, and trusts. The National Taxpayer Advocate Erin Collins described the issue as "widespread and not limited to a small or specialized group of taxpayers."

📋 Step 1: Check Your IRS Transcript

Before you file anything, you need to figure out whether you were actually charged eligible penalties or interest.

The fastest way to do that is through your IRS online account at IRS.gov. Once logged in, look for your tax account transcript for the years 2019 through 2022. You're looking for any penalty or interest charges that were assessed during the period between January 20, 2020, and July 10, 2023.

If you see charges in that window, you may have a claim.

If you don't have an IRS online account, you can request transcripts by mail — though that typically takes five to ten business days, so don't wait too long.

Not sure how to read your transcript? The National Taxpayer Advocate published a step-by-step guide on May 5, 2026, with a worked example showing exactly what to look for. It's available at taxpayeradvocate.irs.gov.

📬 Step 2: File Form 843 Before July 10

If your transcript shows eligible penalties or interest, you'll need to file Form 843 — Claim for Refund and Request for Abatement.

A few important things to know about this form:

- It cannot be filed electronically. You have to mail it on paper.

- The IRS does not confirm receipt. So send it via certified mail, which gives you legal proof that it was submitted before the deadline.

- Write clearly on the top of the form that your claim is "based on the COVID-19 disaster relief period and the legal reasoning reflected in Kwong v. United States," and include the specific penalties, tax period, and dates involved.

If you've already paid the penalties, you're asking for a refund. If you haven't paid them yet and still owe them, you're asking for an abatement — meaning you want the charges reduced or removed.

⚠️ Important: Even if you're not sure whether you qualify, the National Taxpayer Advocate recommends filing a protective claim — essentially a placeholder that is intended to preserve your right to a refund while the courts sort out the issue. Write "Protective Refund Claim Pursuant to Kwong Case" across the top of Form 843, identify the affected tax years and the nature of the penalties, and fill in as much detail as you can. If the ruling ultimately goes in taxpayers' favor, your claim will already be on file.

❓ How Much Could You Get Back?

It varies enormously depending on how much you owed, what kinds of penalties you were charged, and how long they accrued. The IRS assessed more than 120 million penalties against tens of millions of taxpayers between January 2020 and July 2023, according to AP. The IRS previously issued refunds under a narrower 2022 relief program that returned about $1.2 billion to roughly 1.6 million taxpayers. The legal theory in Kwong reaches considerably more taxpayers than that program did — which is why the National Taxpayer Advocate described this as a potential "major refund opportunity."

For some people this might be a few hundred dollars. For small business owners or anyone who had large outstanding balances during the pandemic, it could be considerably more. No one can tell you the exact number without reviewing your specific transcript.

⏰ The Deadline Is July 10. Don't Sit on This.

Most taxpayers will need to file claims by July 10, 2026, using Form 843. That's 59 days from today. Form 843 has to be mailed on paper. Certified mail takes a few days. You need time to pull your transcripts and fill out the form.

The National Taxpayer Advocate has specifically flagged that lower and moderate-income taxpayers — those least likely to have professional tax advisers — are at the highest risk of missing this deadline simply because they don't know about it. This is exactly the kind of situation where being informed is worth actual money.

If you think you might qualify, the time to act is now, not in late June.

Sources

- National Taxpayer Advocate (IRS) — "Tens of Millions of Taxpayers May Be Eligible for Significant Tax Refunds – If They Act by July 10 (Part I)": https://www.taxpayeradvocate.irs.gov/news/nta-blog/tens-of-millions-of-taxpayers-may-be-eligible-for-significant-tax-refunds/2026/04/

- National Taxpayer Advocate (IRS) — "How to Use IRS Tax Account Transcripts to Identify Potential COVID-19 Disaster Relief Refunds (Part II)": https://www.taxpayeradvocate.irs.gov/news/nta-blog/how-to-use-irs-tax-account-transcripts-to-identify-potential-covid-19-disaster-relief-refunds-part-ii/2026/05/

- National Taxpayer Advocate (IRS) — "Protect Your Potential COVID-19 Disaster Relief Refunds By Filing Formal or Protective Claims for Refund (Part III)": https://www.taxpayeradvocate.irs.gov/news/nta-blog/protect-your-potential-covid-19-disaster-relief-refunds-by-filing-formal-or-protective-claims-for-refund-part-iii/2026/05/

- CNBC — "IRS may owe millions of taxpayers refunds for pandemic-era penalty relief. How to file a claim": https://www.cnbc.com/2026/05/11/kwong-v-united-states-tax-refund-deadline.html

- IRS — Form 843, Claim for Refund and Request for Abatement: https://www.irs.gov/forms-pubs/about-form-843

Market Munchies and Mode Mobile communications are for informational purposes only, and are not a recommendation, solicitation, or research report relating to any investment strategy, security, or digital asset. All investments involve risk including the loss of principal and past performance does not guarantee future results.

Any information contained in this commentary does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no guarantee that any statements or opinions provided herein will prove to be correct.