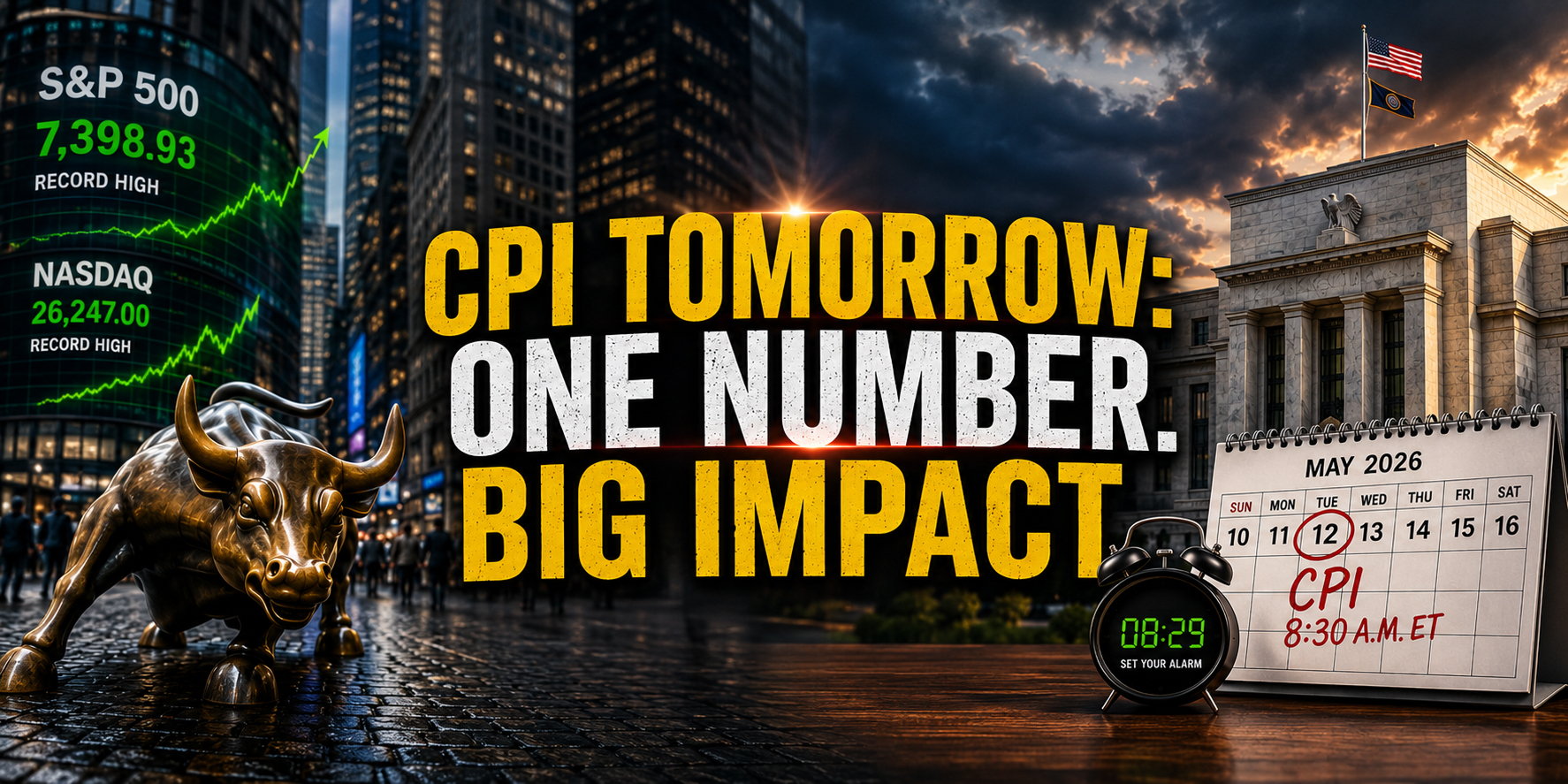

The Stock Market Just Hit an All-Time High. One Number Tomorrow Morning Could Change Everything — But Maybe Not How You Think.

The April CPI report drops at 8:30 a.m. ET Tuesday. Here's how to read it — without panicking. Wall Street threw itself a party last week. The S&P 500 closed Friday at a record 7,398.93, the Nasdaq surged to 26,247, and the rally has now stretched across six straight weeks…

The April CPI report drops at 8:30 a.m. ET Tuesday. Here's how to read it — without panicking.

Wall Street threw itself a party last week. The S&P 500 closed Friday at a record 7,398.93, the Nasdaq surged to 26,247, and the rally has now stretched across six straight weeks — the longest winning streak since 2024. AI chip stocks are flying, jobs data beat expectations for the second month running, and investor sentiment is about as frothy as a cappuccino at a bull market breakfast.

Tomorrow morning at 8:30 a.m. ET, the Bureau of Labor Statistics drops the April Consumer Price Index. Depending on what that number says, the party could keep going — or the music could pause. The key word is pause, not end. Because 2026 has already proven that this market knows how to climb a wall of worry.

🔥 Why This CPI Print Matters More Than Usual

March's report rattled nerves. Consumer prices surged 0.9% in a single month — the biggest jump since June 2022 — driven largely by a 21.2% spike in gasoline prices after the U.S.-Iran conflict disrupted shipping through the Strait of Hormuz. Annual inflation jumped from 2.4% in February to 3.3% in March.

April's data will answer the crucial follow-up question: is that energy shock staying contained in the pump price, or is it bleeding into rent, food, and the services that make up everyday life?

Wall Street consensus is calling for headline CPI at 0.6% month-over-month and 3.7% year-over-year. Core CPI — which strips out food and energy — is expected at 0.3% MoM and 2.7% YoY.

Jennifer Timmerman, Senior Investment Strategy Analyst at Wells Fargo, offered a measured read: "The April CPI report likely will show little to no daylight between wage inflation and consumer-price inflation, setting the stage for a loss of momentum in consumer spending — especially discretionary outlays — in the coming months." (Kiplinger, May 2026)

That's worth watching. It's not a death sentence.

💡 The Numbers That Actually Matter: Know Your Thresholds

Not all hot prints are created equal. Here's the specific data investors should track tomorrow morning — and where things get genuinely dangerous versus merely noisy.

For headline CPI, consensus sits at 0.6% month-over-month and 3.7% year-over-year. That's already elevated, but it's priced in. The danger zone starts above 0.8% MoM — that's the level that would trigger an immediate selloff as traders reprice rate expectations in real time.

Core CPI — which strips out food and energy and is the number the Fed actually obsesses over — is expected at 0.3% MoM and 2.7% YoY. If core comes in above 0.4% MoM, that's the signal investors need to worry about: it means the energy shock is no longer staying in its lane and is spreading into the stickier parts of the economy.

A print that lands at or below consensus is manageable. The market has already priced in elevated energy costs; a number that matches expectations may even be greeted with relief. It's the upside surprises — especially in core — that could send 10-year Treasury yields back toward 4.5% and pressure the high-multiple tech names that have led the rally.

A soft print, on the other hand, is rocket fuel. Yields dip below 4%, rate-cut expectations revive, and analysts who track the index suggest the S&P could push toward 7,584.

🏦 The Fed Factor — And Why It's More Complicated Than It Looks

Here's where the picture gets genuinely interesting rather than just scary.

Jerome Powell's term as Fed Chair ends Thursday, May 15. The Senate is expected to vote on Kevin Warsh's confirmation this week, and markets are watching closely. Three Fed voting members already signaled at the April meeting that they don't support an easing bias — a reminder that the Fed chair doesn't set rates alone.

But Warsh's arrival matters. He has argued publicly that AI-driven productivity gains create room to cut rates without stoking inflation — a view more optimistic than Powell's. And with President Trump applying consistent public pressure for rate cuts, a new chair who shares even a fraction of that disposition could change the calculus faster than any single CPI print.

Bank of America has pushed its first expected rate cut all the way to the second half of 2027. JPMorgan's models show inflation likely staying above 2% through early 2027 in most scenarios. These are reasonable forecasts — but they were built before Warsh takes the chair on Thursday. The "Trump Factor" is real, and it introduces upside uncertainty that the purely data-driven models don't fully capture.

The NY Fed's April Survey of Consumer Expectations found one-year inflation expectations at 3.6%, the highest in a year — a number the Fed watches carefully. But the same survey showed longer-term expectations (3- and 5-year) holding steady at 3.1% and 3.0%, suggesting households aren't expecting this to become a permanent condition.

📊 Is 20.9x Forward P/E Actually That Scary?

The S&P 500 is trading at 20.9 times forward earnings — elevated by historical standards, but not inexplicable in context. The last time AI drove a genuine productivity step-change across the economy, valuations re-rated dramatically and stayed there longer than skeptics expected.

Tech giants Amazon, Alphabet, Microsoft, and Meta are collectively planning to spend almost $700 billion on AI infrastructure in 2026 — not to get ahead of demand, but to keep up with existing customer commitments. That's not speculative. That's contracted capital expenditure. When the earnings are real and the growth is real, "expensive" doesn't automatically mean "about to crash."

The risk isn't that the market is wrong about AI. The risk is that a hot inflation print forces higher rates that make those future earnings worth less in today's dollars. That's a valuation math problem, not a business fundamental problem — and it's the kind of thing that can resolve itself as energy prices normalize.

🗓️ The Rest of the Week Is Equally Loaded

Tuesday's CPI isn't the only dish being served this week. The full menu:

- Wednesday: Producer Price Index (PPI) + Cisco earnings — a direct proxy for enterprise AI spending

- Wednesday: Alibaba earnings — a major test for China tech sentiment ahead of the summit

- Thursday/Friday: Trump-Xi summit in Beijing — the outcome could move semiconductor and trade-sensitive names sharply in either direction

- Thursday: Kevin Warsh's expected Senate confirmation vote; Powell's final day as Chair

The Trump-Xi meeting deserves its own spotlight. Any expansion of the existing 90-day trade truce — or, better, a signal on tariff reductions — could send Amazon, Meta, and Qualcomm surging again, just as they did when the truce was first announced. A breakdown, on the other hand, would be a fresh headwind for tech.

🍽️ The Bottom Line

This market has earned its record highs. Six weeks of gains built on real earnings, real AI capex, and a jobs market that keeps outperforming are not nothing. The "wall of worry" — Iran, inflation, a Fed leadership change — is real, but so is the economy climbing it.

Tomorrow's CPI is the most important single data point of the week. But one number rarely tells the whole story. If the print is hot but below the danger thresholds above, the rally likely digests it and moves on. If core CPI comes in above 0.4% MoM and Warsh's confirmation runs into trouble at the same time — that's the scenario where the soufflé truly burns.

Use this week as a risk-management checkpoint, not a panic trigger. Check your stop-losses on high-multiple AI names. Make sure you know why you own what you own. And set your alarm for 8:29 a.m. Tuesday.

Sources

- CNBC — "Nasdaq's Record Run Faces a CPI Test After AI Chip Stocks and Jobs Data Lift Wall Street" (May 10, 2026): https://ts2.tech/en/nasdaqs-record-run-faces-a-cpi-test-after-ai-chip-stocks-and-jobs-data-lift-wall-street/

- Kiplinger — "What to Expect From the April CPI Report" (May 2026): https://www.kiplinger.com/investing/economy/cpi-report-april-2026-what-to-expect

- U.S. Bureau of Labor Statistics — CPI Home (April 2026 release schedule): https://www.bls.gov/cpi/

- FX Leaders — "S&P 500 & Nasdaq 100 Weekly Outlook: Record Highs Meet the Week That Decides the Fed Path" (May 10, 2026): https://www.fxleaders.com/news/2026/05/10/sp-500-nasdaq-100-weekly-outlook-record-highs-meet-the-week-that-decides-the-fed-path/

- Federal Reserve Bank of New York — April 2026 Survey of Consumer Expectations (May 7, 2026): https://www.newyorkfed.org/newsevents/news/research/2026/20260507

- TradingKey — "U.S. April CPI Preview" (May 2026): https://www.tradingkey.com/analysis/economic/inflation/261877612-cpi-bls-april-oil-consumer-inflation-fed-nonfarm-rate-interest-jpm-tradingkey

- CNN Business — "Powell confirms he will step aside at end of his term as chair but remain on the Fed's board" (April 29, 2026): https://www.cnn.com/2026/04/29/business/live-news/federal-reserve-interest-rate

- GoTrade — "US Market Outlook May 11–15 2026: CPI Is Key" (May 11, 2026): https://www.heygotrade.com/en/news/weekly-economic-outlook-2026-05-11/

- The Motley Fool — "Prediction: AI Infrastructure Stocks Will Crush the S&P 500 in 2026" (May 10, 2026): https://www.fool.com/investing/2026/05/10/prediction-ai-infrastructure-stocks-will-crush-the/

- Trading Economics — United States Inflation Rate: https://tradingeconomics.com/united-states/inflation-cpi

Market Munchies and Mode Mobile communications are for informational purposes only, and are not a recommendation, solicitation, or research report relating to any investment strategy, security, or digital asset. All investments involve risk including the loss of principal and past performance does not guarantee future results.

Any information contained in this commentary does not purport to be a complete description of the securities, markets, or developments referred to in this material. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete. There is no guarantee that any statements or opinions provided herein will prove to be correct.